E-commerce in Europe is entering a decisive phase. What began as a convenient alternative to physical retail has now become a dominant force shaping how consumers shop, pay, and interact with brands. E-commerce payment trends 2026 According to Forrester, online retail sales across the five largest European economies—France, Germany, Italy, Spain, and the UK—are forecast to grow at a compound annual growth rate (CAGR) of 7.8% over the next five years. By 2029, nearly one-fifth of all retail spending in these markets is expected to happen online, up from around 16% in 2024.

These figures make one thing clear: by 2026, digital commerce will be more embedded in everyday life than ever before. With that growth comes rising consumer expectations. E-commerce payment trends 2026 Shoppers no longer tolerate slow checkouts, confusing authentication steps, or delayed refunds. They expect payments to be instant, intuitive, and secure—almost invisible in the buying journey.

To meet these demands, merchants, payment providers, and financial institutions are rethinking how payments work at every stage of the customer experience. E-commerce payment trends 2026 From digital wallets and bank-to-bank payments to AI-driven commerce and digital identity frameworks, the next wave of payment innovation is redefining what “good checkout” really means.

Here are the six most important e-commerce payment trends set to shape the European market in 2026 and beyond.

1. Digital Wallets Strengthen Their Role as the Default Payment Choice

Digital wallets are no longer just an alternative payment option—they are becoming the foundation of modern online checkout. In 2026, wallet-based payments are expected to account for an even larger share of e-commerce transaction value, driven by consumer demand for speed, simplicity, and trust.

Services such as Apple Pay, Google Pay, and PayPal have succeeded because they remove friction from the buying process. E-commerce payment trends 2026 Instead of entering card details, billing addresses, and security codes, customers can complete a purchase in seconds using biometric authentication or a single tap. E-commerce payment trends 2026 This streamlined experience directly addresses one of e-commerce’s biggest challenges: cart abandonment.

A major reason behind the popularity of digital wallets is their seamless alignment with existing consumer behaviour. Debit cards remain a preferred payment instrument in many European countries, but their traditional online usage can be cumbersome. E-commerce payment trends 2026 E-commerce payment trends 2026 By storing debit cards inside trusted wallet apps, consumers effectively bypass those barriers.

As Manfred Schulz, Head of Merchant Solutions at Brite, explains, debit cards have found new life through wallets. Consumers simply add their cards to platforms like Apple Pay or PayPal and use them effortlessly online. E-commerce payment trends 2026 In countries such as Germany—where cashless adoption continues to rise—digital wallets are becoming an essential checkout option rather than a value-add.

Beyond convenience, wallets also offer built-in security features such as tokenisation, biometric verification, and advanced fraud prevention. For consumers, this creates confidence. For merchants, it reduces fraud risk while increasing conversion rates.

At the same time, the rise of Pay by Bank solutions mirrors the same consumer desire for simplicity. While these solutions have not yet reached wallet-level adoption, E-commerce payment trends 2026 they are gaining momentum because they do not require new apps or complex onboarding. Customers pay directly through their existing banking interface, maintaining control and familiarity.

By 2026, the distinction between wallets and bank-based payments will matter less than the shared principle driving both: fast, secure, and frictionless checkout. Merchants that prioritise wallet-first strategies will be better positioned to meet customer expectations in an increasingly competitive digital landscape.

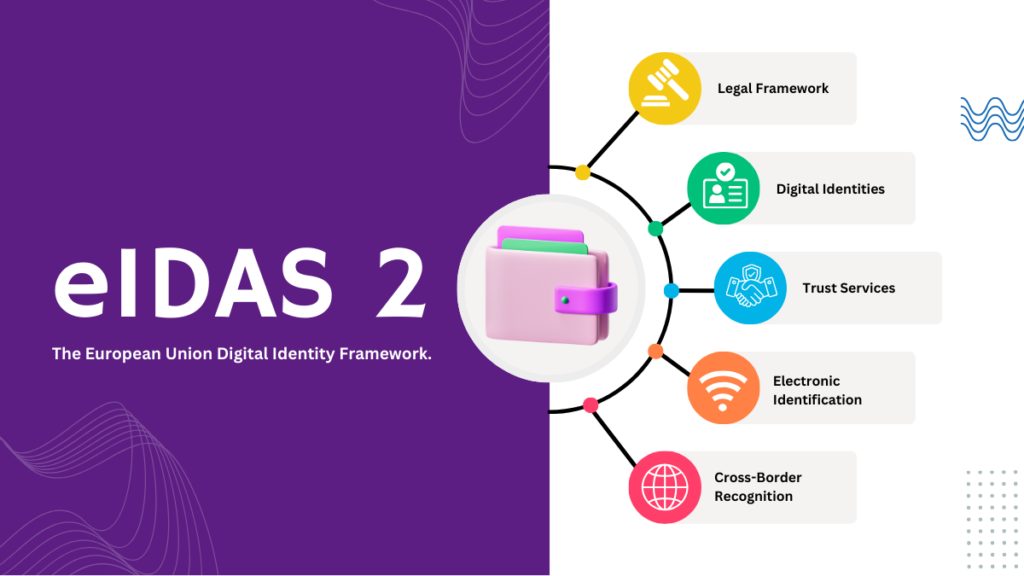

2. eIDAS 2.0 Redefines Digital Identity and Online Verification

Although the updated eIDAS regulation does not directly govern payments, its impact on European e-commerce will be profound. eIDAS 2.0 introduces a unified framework for digital identity, authentication, and trust services across the European Union—fundamentally changing how consumers prove who they are online.

At the heart of this transformation is the European Digital Identity Wallet (EUDIW). By November 2026, all EU Member States must provide citizens with access to this government-backed digital wallet. The EUDIW allows users to securely store and share verified personal credentials, creating a standardised identity solution across borders.

For e-commerce, this opens the door to dramatically smoother checkout and onboarding experiences. Instead of repeatedly creating accounts or uploading documents, shoppers can authenticate themselves instantly using trusted credentials. This reduces friction while strengthening security and fraud prevention.

The EUDIW also introduces the concept of verifiable credentials, which enables selective data sharing. For example:

- Age verification becomes instant and privacy-friendly. Customers can prove they are over 18 when buying regulated products without revealing their full date of birth.

- Minimal data exposure ensures that shoppers only share what is strictly necessary, reducing the risk of data breaches.

- Expanded credentials, such as IBAN verification or proof of education, could support faster account setup, personalised offers, and improved credit or payment decisions.

As these capabilities mature, identity and payments will become increasingly interconnected. A trusted digital identity framework reduces fraud, improves compliance, and builds consumer confidence—key ingredients for scalable e-commerce growth.

By 2026, merchants that integrate eIDAS-compliant identity solutions will be well-positioned to deliver faster, safer, and more user-friendly shopping experiences.

3. Buy Now, Pay Later Enters a Phase of Regulated Maturity

Europe has long been a global hub for Buy Now, Pay Later (BNPL) innovation. With companies like Klarna leading the way, E-commerce payment trends 2026 instalment payments have become a popular alternative to credit cards—especially in markets where revolving credit is less common.

BNPL continues to perform strongly because it aligns with European consumer preferences for transparency and controlled spending. Instead of open-ended credit, shoppers can spread costs across clear, fixed instalments.

However, the rapid expansion phase of BNPL is giving way to a more regulated and sustainable model. Under the revised EU Consumer Credit Directive (CCD II), many BNPL products will fall under stricter consumer credit rules by 2026. Countries such as the Netherlands are already moving in this direction.

These changes will introduce enhanced affordability checks, clearer disclosures, and stricter marketing guidelines—particularly to protect vulnerable consumers. While this may slow growth in the short term, it also strengthens trust and legitimacy across the sector.

Rather than weakening BNPL, regulation is expected to stabilise it. Providers will focus on responsible lending, improved risk management, and long-term customer relationships. For merchants, this means offering BNPL as a trusted payment option rather than a high-risk conversion tool.

By 2026, BNPL will no longer be defined by rapid expansion alone, but by credibility, compliance, and consumer confidence.

4. Pay by Bank Expands Beyond Early Adopters

Account-to-account (A2A) payments—commonly referred to as Pay by Bank—are rapidly gaining ground across Europe. Supported by regulatory initiatives such as the Instant Payments Regulation (IPR), these payment methods allow consumers to pay directly from their bank accounts without card networks.

For merchants, the benefits are compelling. Pay by Bank eliminates card processing fees, reduces chargeback risk, and delivers real-time settlement. Instead of waiting days for funds to clear, merchants receive confirmation immediately, allowing faster order processing and improved cash flow.

Consumer adoption is also accelerating. The German market provides a clear example of this shift:

- High retention: Three-quarters of users who try Pay by Bank plan to use it again.

- Key motivators: Security, low fees, and ease of use consistently rank as top drivers.

- Consumer priorities: Zero fees and fast refunds are often valued more than real-time balance updates.

Interestingly, refund speed is emerging as a critical factor in payment choice. Many consumers prefer knowing their money will return quickly in case of a return or cancellation—even more than seeing instant balance updates.

As awareness grows and user experiences improve, Pay by Bank is moving beyond niche use cases and entering the mainstream. By 2026, it is expected to be a core payment method across demographics, not just among digitally savvy consumers.

5. Instant Refunds Become a Baseline Expectation

As instant payments become more common, consumer expectations around refunds are changing just as quickly. In 2026, waiting several days for a refund will feel outdated—especially in markets where real-time payments are widely available.

Technological advances now allow refunds to be processed independently from the original payment method. Solutions like instant A2A payouts enable merchants to return funds directly to customer bank accounts within seconds.

Consumer data supports this shift. In Germany, nearly half of shoppers expect refunds to arrive within one minute of initiation. At the same time, SEPA Instant Payments infrastructure has proven its reliability, with the vast majority of transactions settling almost immediately.

For merchants, instant refunds offer more than just customer satisfaction. They reduce support enquiries, streamline returns management, and reinforce brand trust. A fast refund can often turn a negative experience into a positive one.

By 2026, instant refunds will no longer be a competitive differentiator—they will be a standard requirement in European e-commerce.

6. AI Agents and Embedded Payments Reshape Online Commerce

Perhaps the most transformative trend on the horizon is the rise of agentic commerce. AI agents are evolving from simple recommendation tools into autonomous actors capable of completing purchases on behalf of consumers.

These agents can identify needs, compare products, negotiate prices, and execute transactions—often without direct human input. The shopping journey becomes intent-driven rather than step-based.

The economic potential is enormous. McKinsey estimates that agent-driven commerce could generate trillions of dollars globally by 2030. Unlike previous digital revolutions, this shift can happen rapidly because AI agents operate on existing infrastructure.

For businesses, this creates both opportunity and urgency. Companies will need to integrate new protocols, rethink identity and trust models, and adapt loyalty programs to an agent-driven world. Embedded payments will play a crucial role, allowing AI systems to transact securely and seamlessly.

Those who adapt early will gain strategic advantage. Those who delay risk becoming invisible to AI-mediated purchasing decisions.

The Future of E-Commerce Payments: 2026 and Beyond

As European e-commerce continues its rapid expansion, payments are no longer just a technical necessity—they are a defining part of the customer experience. Digital wallets, Pay by Bank, regulated BNPL, instant refunds, digital identity, and AI-powered commerce are converging to create a faster, smarter, and more trustworthy ecosystem.

Looking ahead, success will depend on integration and adaptability. Consumers expect convenience without compromising security. Merchants must reduce friction, manage costs, and stay ahead of regulatory change.

Global Payments Releases its 2026 Commerce and Payment Trends Report – Comprehensive insights on the key trends shaping commerce and payment experiences globally in 2026. Global Payments 2026 Commerce & Payment Trends Report