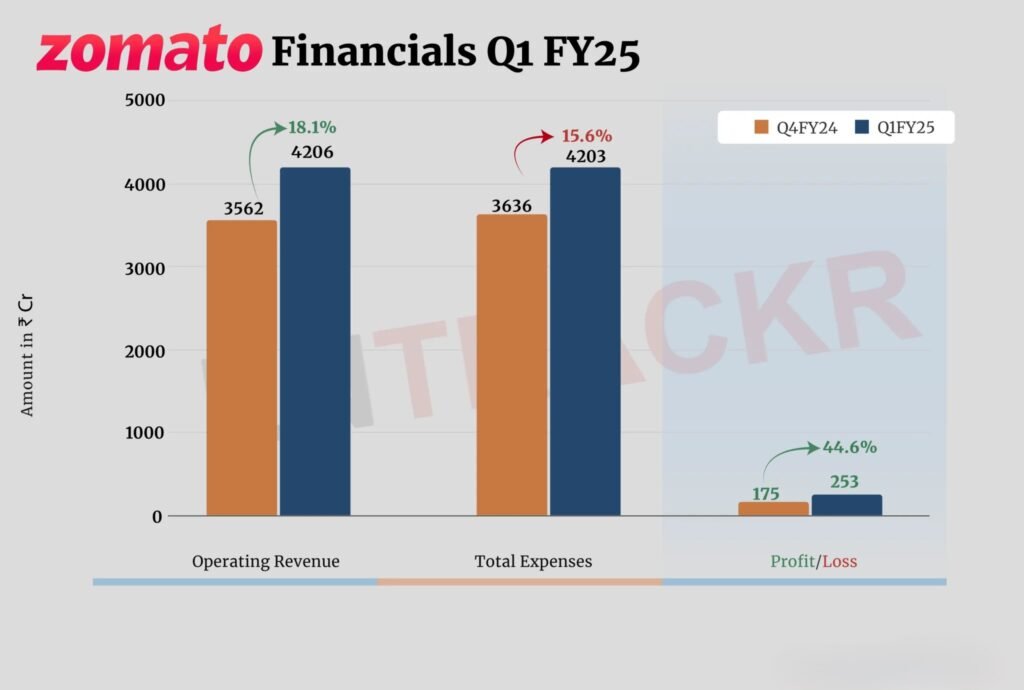

Zomato’s parent company, Eternal, has quietly transformed itself from a food delivery app into one of India’s most complex consumer commerce ecosystems. According to the latest figures, the Zomato Revenue Model: Eternal’s Multi-Vertical Profit Engine generated operating revenue of approximately ₹20,243 crore in FY25, up sharply from ₹12,114 crore in FY24. Net profit rose to ₹527 crore, marking a near 50% year-on-year increase, while revenue surged 67% YoY.

These numbers are not accidental. They reflect a carefully layered monetization strategy across food delivery, quick commerce, B2B supply chains, subscriptions, and advertising. For founders and platform entrepreneurs, studying the Zomato Revenue Model: Eternal’s Multi-Vertical Profit Engine offers a real-world blueprint for building diversified, scalable, and defensible revenue models.

This article breaks down how Zomato actually makes money, what each vertical contributes, where profits come from, where losses still exist, and the key lessons new platform builders—especially those launching Zomato-like apps—can apply.

Zomato (Eternal) FY25: The Big Picture

In FY25, Eternal delivered its strongest financial performance since listing.

Key Financial Highlights

- Operating Revenue (FY25): ~₹20,243 crore

- Operating Revenue (FY24): ~₹12,114 crore

- Year-on-Year Growth: ~67%

- Net Profit (FY25): ~₹527 crore

- Adjusted EBITDA: ~₹1,079 crore (vs ~₹372 crore in FY24)

Quarterly performance was equally revealing. In Q4 FY25, operating revenue rose 64% YoY to ~₹5,833 crore, although quarterly net profit dipped to ~₹39 crore due to heavy investments in Blinkit, dark store expansion, and logistics.

The takeaway is clear: Zomato is prioritizing long-term dominance over short-term quarterly profits.

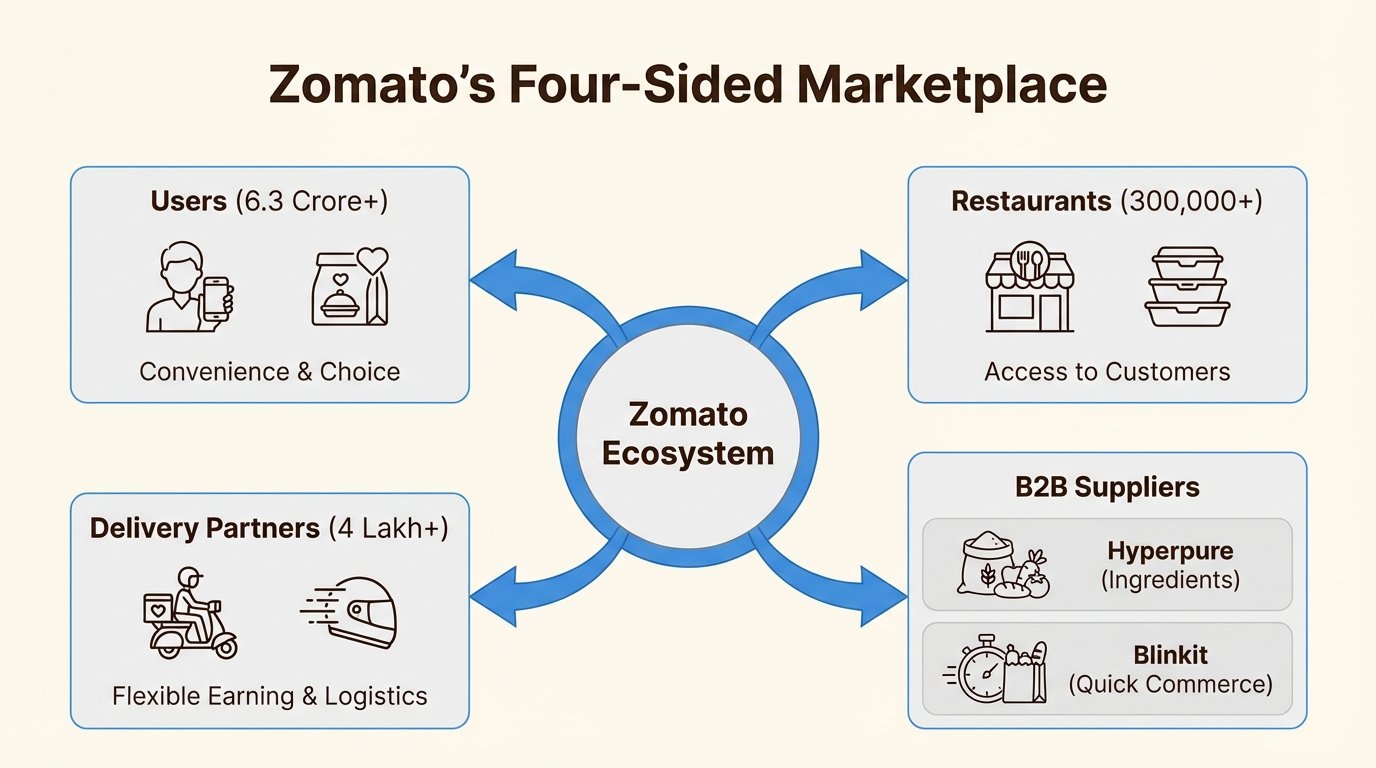

From Food App to Commerce Ecosystem

Zomato is no longer a single-vertical business. Today, Eternal reports revenue across four major business lines:

- Food Delivery

- Quick Commerce (Blinkit)

- B2B Supply Chain (Hyperpure)

- Going-Out / Lifestyle Services

This shift has reduced dependency on food delivery alone and allowed Zomato to extract value from both sides of the marketplace—consumers and businesses.

Revenue Breakdown by Vertical (FY25)

Approximate adjusted revenue contribution in FY25:

| Vertical | FY25 Revenue |

|---|---|

| Food Delivery | ~₹9,418 crore |

| Blinkit (Quick Commerce) | ~₹5,206 crore |

| Hyperpure (B2B Supply) | ~₹6,196 crore |

| Going-Out / District | ~₹737 crore |

Food delivery remains the foundation, but Blinkit and Hyperpure together now account for more than half of total revenue, signaling a major structural shift.

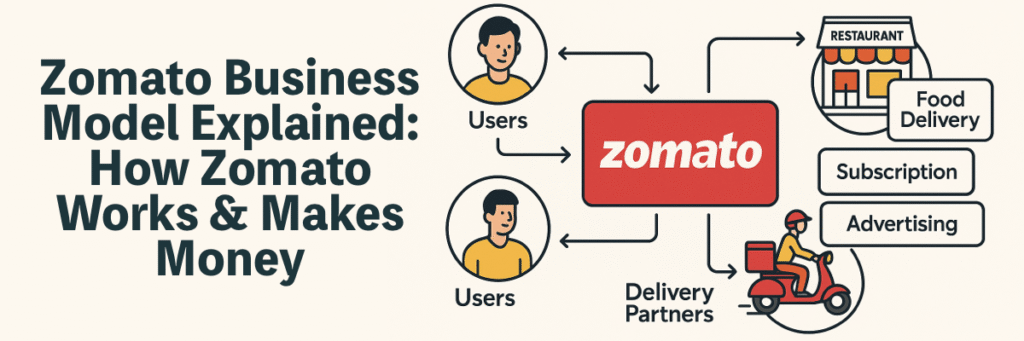

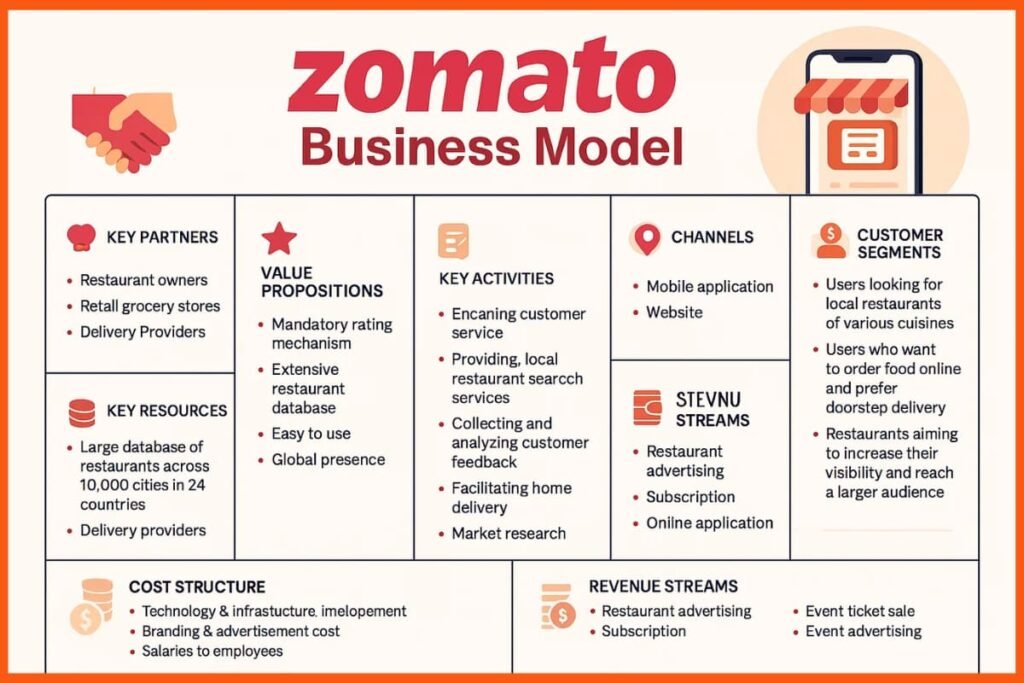

Revenue Stream #1: Food Delivery Commissions (The Core Engine)

How It Works

When a customer places a food order, Zomato charges the restaurant a commission (take rate) on the order value. This is the classic marketplace model—Zomato facilitates discovery, ordering, payments, and delivery.

Take Rates & Pricing

- Typical commission: 20–25%

- Additional charges for:

- Sponsored listings

- Priority placement

- Promotional campaigns

- Faster delivery slots

Contribution to Revenue

Food delivery contributes 25–35% of total operating revenue, making it the most stable and profitable vertical.

Scale Advantage

In FY25:

- Total orders: ~853 million

- Average order value: ~₹453

Even marginal increases in AOV or frequency have a massive impact at this scale.

Why It’s Profitable

- High order density

- Predictable demand

- Strong brand recall

- Improving delivery efficiency

Food delivery remains Zomato’s profit anchor, funding expansion into newer verticals.

Revenue Stream #2: Blinkit (Quick Commerce)

Blinkit represents Zomato’s bet on instant consumption.

How Blinkit Makes Money

- Product markups (thin margins)

- Delivery fees

- Platform convenience fees

- Brand advertising & sponsored placements

FY25 Performance

- Revenue: ~₹5,206 crore

- YoY growth: ~126%

- AOV: Increased from ~₹613 to ~₹667

- Adjusted EBITDA loss: Narrowed to ~₹292 crore

Why Losses Persist

Quick commerce is capital-intensive:

- Dark store rentals

- Inventory holding

- High rider density

- Perishable goods wastage

However, as order density increases and idle capacity reduces, margins are steadily improving.

Blinkit is not yet a profit engine—but it is becoming a strategic moat.

Revenue Stream #3: Hyperpure (B2B Supply Chain)

Hyperpure supplies fresh produce, staples, and kitchen essentials to:

- Restaurants

- Cloud kitchens

- Blinkit dark stores

How It Generates Revenue

- Markups on wholesale supplies

- Logistics and delivery charges

- Volume-based pricing contracts

FY25 Performance

- Revenue: ~₹6,196 crore

- YoY growth: ~95%

- Adjusted EBITDA loss: Reduced to ~₹84 crore

Margins are thin, but Hyperpure plays a critical role:

- Improves restaurant loyalty

- Enables better cost control

- Strengthens supply chain integration

Hyperpure may never be highly profitable—but it stabilizes the ecosystem.

Revenue Stream #4: Subscriptions & Loyalty Programs

Zomato’s subscription programs (Gold / Plus) drive:

- Higher order frequency

- Lower churn

- Predictable recurring revenue

Pricing

- ₹399 to ₹1,200 per year (varies by city)

- Benefits include:

- Free delivery

- Cashback

- Exclusive deals

- Priority access

Revenue Impact

Subscriptions contribute an estimated 8–12% of total revenue, but their real value lies in boosting lifetime value (LTV).

A subscribed user typically orders 4–5x more frequently than a casual user.

Revenue Stream #5: Advertising & Promotions

Advertising is Zomato’s highest-margin revenue stream.

Who Pays?

- Restaurants

- FMCG brands

- Beverage companies

- Local merchants

Ad Formats

- Sponsored listings

- Banner ads

- Search prioritization

- Category dominance

Revenue Contribution

Advertising accounts for roughly 5–10% of revenue, but contributes disproportionately to gross profit due to low incremental costs.

As platform traffic grows, ad monetization becomes increasingly powerful.

Approximate Revenue Mix (FY25)

| Revenue Stream | Share |

|---|---|

| Food delivery commissions | 25–35% |

| Blinkit (quick commerce) | 20–30% |

| Hyperpure (B2B supply) | 25–35% |

| Subscriptions | 8–12% |

| Advertising | 5–10% |

Fee Structure: Who Pays What?

User-Side Fees

- Delivery charges

- Surge pricing during peak hours

- Convenience/platform fees

- Subscription fees

Restaurant-Side Fees

- Commission (20–25%)

- Advertising & promotion charges

- Onboarding or listing fees

- Cancellation penalties

Hidden Monetization

- Float income on held funds

- Data & analytics insights

- Brand co-funded discounts

- Cross-subsidization across verticals

This multi-layered fee architecture allows Zomato to extract value without overburdening any single stakeholder.

How Zomato Increases Revenue Per User (ARPU)

Zomato doesn’t rely on volume alone—it actively optimizes user value.

Key Strategies

- User segmentation (casual vs heavy users)

- Subscription upselling

- Cross-selling Blinkit to food users

- Dynamic delivery pricing

- Bundled offers (“add dessert for ₹49”)

- Personalized recommendations

A heavy user might place 40+ orders per year, compared to fewer than 10 for a non-subscriber.

Cost Structure & Margin Reality

Major Cost Centers

- Delivery rider payouts

- Marketing & discounts

- Technology infrastructure

- Warehousing & dark stores

- Customer support & operations

In FY25:

- Delivery costs rose ~46% YoY

- Marketing expenses jumped ~38%

Food delivery is margin-positive, while Blinkit and Hyperpure remain loss leaders aimed at long-term dominance.

Zomato vs Competition

- Food delivery market share: ~55–58%

- Swiggy: ~42–45%

- Blinkit competes aggressively with Instamart and Zepto

- Cross-vertical integration gives Zomato a structural advantage

Few competitors operate both consumer and supply-side verticals at this scale.

Future Revenue Opportunities (2025–2027)

Potential growth drivers include:

- Premium subscription tiers

- Sponsored delivery speed

- Data & analytics monetization

- Financial services for restaurants

- Cloud kitchen infrastructure

- AI-powered ad optimization

Advertising and subscriptions are expected to account for a larger share of profits, even if transaction margins remain thin.

Lessons for Entrepreneurs & Platform Builders

Zomato’s success offers clear takeaways:

- Start with a strong core marketplace

- Achieve unit-level efficiency before expanding

- Add adjacent verticals gradually

- Monetize attention via ads

- Use subscriptions to stabilize revenue

- Avoid capital-heavy models too early

For startups, lighter clones can outperform giants by:

- Targeting niche markets

- Focusing on Tier-2/3 cities

- Running ad-heavy, low-commission models

- Avoiding inventory risk initially

For a deep dive into how digital food delivery platforms like Zomato make money (commissions, subscriptions, advertising, logistics, supply), see this business model overview of Zomato’s revenue streams. Decoding Zomato Business Model: Revenue Streams, Operations, and Future

For more context on how quick commerce strategies like Blinkit’s are evolving within such revenue models, check out our in‑depth Blinkit article here: Blinkit drops 10‑minute delivery claim (SmallSEOKit)